Sanction Screening

Using Zero Knowledge Proofs for Sanctions Screening

Mechanism proposed by TRISA suggests implementing a zero-knowledge proof based solution to perform sanctions screening. It works in the following manner. Each VASP generates a proof of non-membership in a sanctions list of its user, i.e., Alice’s VASP generates a proof claiming Alice does not belong to a sanctions list, and Bob’s VASP for Bob As shown in the picture below, these proofs are exchanged and verified by the two VASPs. By verifying that a proof is valid, a VASP can ensure that the counterparty does not belong to a sanctions list, and thereby fulfil its obligation.

The proof consists of two sub-proofs; the first is a proof to show a user’s KYC AML data is not on the sanctions list. The second proof shows that the KYC AML data used for the proof is the same one as encrypted under the regulator’s key (to be saved for when a regulator, such as OFAC or FINCEN, wishes to look up a particular user).

Both VASPs only make transactions once they’ve ensured due diligence is done. Data is still stored for regulators. All VASPs learn user information on a need-to-know basis, so the breach of Bob’s VASP database does not compromise Alice’s data. Each transaction contains an additional audit trail recording the version of the sanctions list used. Full confidentiality over communication channels for sanction checks.

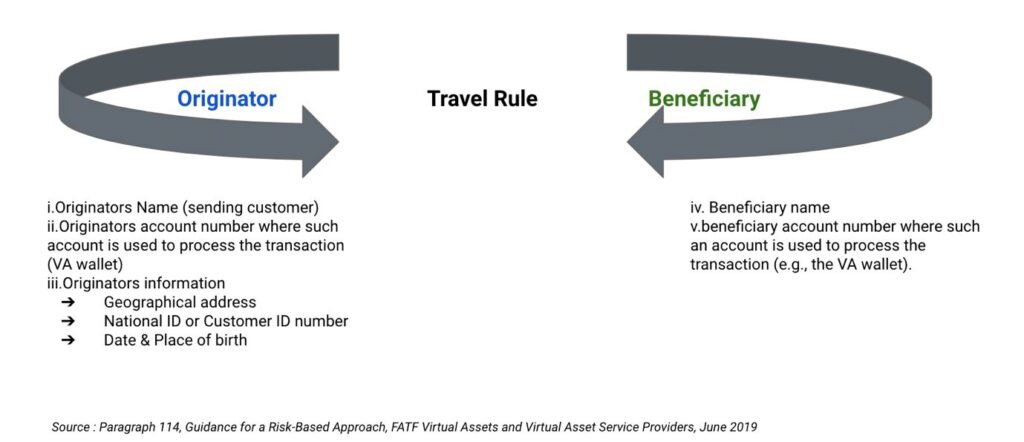

Travel Rule information sharing architecture

iv. VA Transfers to/from unhosted wallets

The FATF standards require VASP’s to obtain the requisite originator and beneficiary information from their customers, as it is not feasible to obtain the relevant information from another VASP.

The standards also prescribe that VASP’s should collect data on their unhosted wallet transfers, monitor and risk assess the information to determine if the transactions are within the risk appetite and the appropriate risk-based controls to apply to such transactions/individual customers and meet SAR obligations.

Similar standards would apply to risks posed by VASP’s that are not yet licensed /registered and supervised for AML/CFT purposes, as they are based in jurisdictions that have not yet implemented the FATF standards for VA’s/VASP’s.

The VASP’s may choose to impose additional controls on transactions with unhosted wallets. Potential measures include;

- Enhancing the existing risk-based control framework to account for specific risks posed by unhosted wallets; and

- Studying the feasibility of accepting transactions only from/to VASP’s and other obliged entities, and/or unhosted wallets that the VASP has assessed to be reliable.

v. Travel Rule Solution Providers

The solution providers should enable VASP’s to carry out the following main functions;

- Enable a VASP to locate a counterparty VASP’s for VA transfers;

- Enable the submission of required and accurate originator and beneficiary information immediately when a VA transfer is conducted on the platform;

- Enable VASP’s to submit large volumes of transactions in an effectively stable manner;

- Enable a VASP to securely transmit data, i.e., protect the integrity and availability of the required information to facilitate record keeping;

- Protect the use of such information by receiving VASP’s as well as to protect it from unauthorized disclosures in line with data protection laws;

- Provide VASP with a communication channel to support further follow up with a counter party VASP for the purpose of;

- Due Diligence on the counterparty VASP

- Requesting additional information on certain transactions to determine if the transactions involve high risk or prohibited activities.

Compliance Program

VASP’s and other obliged entities are required to maintain AML/CFT programs and systems to adequately manage and mitigate their risks.

SAR Reporting and Tipping Off

VASP’s are required to implement appropriate systems for scrutinizing transactions in a time manner and determining whether funds or transactions are suspicious. The lack of required originator and beneficiary information should be considered as a factor in assessing whether a transfer is suspicious and if it is required to be reported.

Where a VASP requests further information on a counterparty from its customer in the case of a transfer from an unhosted wallet, it should expect its customers to respond in a timely fashion and provide documents/information to the level of detail requested. Where the customer does not respond, it may trigger concerns and should lead the VASP to consider filing a SAR on their customer. It should be followed by a reassessment of the customer’s attributes and risk profile when necessary.

The obligation for VASP’s to report suspicious transactions is not risk based. Suspicious funds and transactions are required to be reported promptly to respective jurisdictional authorities.

NIMBL will be happy to advise you on the Travel Rule & Anti Money Laundering Framework Requirements.